Digital Business Transformation

Identify and realize opportunities

Reading time approx. 14 mins

Business models are changing

What does it mean, when a company is reporting quarter after quarter a setback in its blockbuster turnover of more than 20%? Generally this are signs of a disaster for that company. Luckily Apple has, thanks to 10 years of successful iPhones sales piled a cash buffer of 130 bn USD and therefor seems to be quiet robust, to cope with such a slump in sales.(1)

However, figures clearly outline the message: Golden days of iPhone premiums are over. After more than 10 years customer do not see much added value anymore in owning an iPhone over even more feature rich competitive alternatives. The iPhone premium is eroding.

Luckily Apple understood! The growth in wearables and services not yet compensate the losses in iPhone sales but the direction fits. And these devices offer a new platform, being even closer at the customers. While the phone is to transfer into a watch, the iPad is positioned to take control over all other iPhone related tasks. Those still investing into phones may already have missed the trend. Foldable screens may sound like an interesting alternative, but whether they will survive users acceptance tests is still to be awaited. If I remember the daily newspaper origami in London tubes during rush hours in the late 1990s, I’ld rather doubt.

However, this picture drastically unveils the change demand and technologies undergo over time. Business models need to adopt to these changes. If not adjusted early enough, the business faces the threat of running obsolete. Today’s excellent value propositions will erode or implode in th ecourse of time.

The value migration within industries fastens, thus the lifetime of business Models keeps to shrink

While IBM charged – ten years ago – its customers a WebSphere application server license around 1,000 USD per core, today nobody would even pay a dime for such a service. The same is about to happen with databases and many other technologies that have been relevant assets to every corporate IT portfolio. Open Source but also technical achievements and simply evolution have created a magnitude of alternatives and substitutions.

Jack Welch, who lead and grew GE between 1981 and 2001 from 27bn to over 130bn turnover, understood during the eighties, that selling excellent machinery respectively jet engines alone, is not making customers happy. Even the most technically optimized engines will not be as valuable to a customer as an engine which is always in operation.(2) Based on this understanding he transformed GE from a machine manufacturer to a service company, that not only earned with the production of the engines but also by operating them. The change from product focus to customer focus served the company sustainable revenue streams for along period of time.

Today’s protagonists – say Amazon or Apple – of this (digital) change are more consumer focused: Think the business from the customer. Give the customer what makes him lucky: free delivery, carefree shopping, simple ordering (

Die heutigen Vorreiter dieses (digitalen) Wandels finden sich im Consumer-Bereich in Form von Amazon oder Apple: Denke das Geschäft vom Kunden; Gib ihm, was ihn glücklich macht: kostenfreie Lieferung, sorgenfreies Shopping, effortless ordering (dash buttons, Alexa), favorite music and entertainment. Meanhwile keep learning and generate customer insight.

In the B2B arena Internet of Things (IoT) based business models promise such kind of bonding: Surveil utilization, analyze behavior and identify new demands respectively sources of additional revenues.

DIgital busines models focus the customer and create a value add relationship

Steve Jobs on “customer focus”, 1997 when he returned to Apple

(click to play)

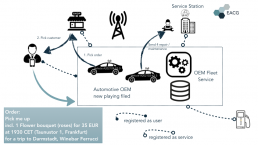

While so far Leaseplan and comparable companies have been useful as fleet managers, new IoT based utilization analysis will allow preventive maintenance concepts. Thus information on repair and maintenance will be first at the car manufacturer. Combined with the autonomous drive option the the vehicles may be directed situation specific either to the next (contracted) service station or another pickup-job.

If OEMs throw the traditional transaction based compensation model over board and start thinking the business from the customer, they might end up, using their market position to form the next generation mobile trading platform. The current model will die in favor of a mobility subscription.

OEM new playing fields (sample vision)

From a customer’s point of view this might be a comfortable scenario, as the value-destroying purchase costs will diminish. While only a lump sum per kilometer will be charged, no further management of inspections, tire replacement or other potential maintenance needs to be taken care of. Not even checking for a parking lot will be necessary any more! All could be self-managed by the vehicle through IoT-based measuring, analysis and orchestration (I am already unpatiently awaiting it!)

In the same time the OEM gains the option, to accompany their customers wherever they go – via app on their mobile. They may study their customers usage, behavior, preferences, movements – routes, frequencies – as well as the actually required demand – SUV, Mini, etc. – or even foreign-brand-usage.

The impact such changes will have on the overall ecosystem are enormous and require extensive research and analysis: The changes in compensation will effect the cash flow. The turnover will spread across the complete customer lifecycle instead a relatively early point in time. The risk of ownership moves from buyer to producer respectively operator. But in the same time a gigantic cosmos of after sales and added value services opens up, if the sales platform “car” can be established (see. picture below). All these challenges are solvable. But the resolution requires a consistent, consolidated change on several levels (operating companies, financing concepts, assurances, technical platfrom,…)

This little sample clearly shows that a serious Digital Transformation is a massive investment and a challenging endeavor consisting of many facets. It definitely requires dedicated senior sponsorship. Existing organizations with their fragmented responsibility schemes might be overcharged by the kind of multi dimensional approach required to cope with such a challenge. On the one hand members of the organization were reqiuired to learn how to operate in the existing, tailored structures. On the other hand the specialized, tailored thinking prevents the whole picture to bee seen clearly. The article on organization and staff will address this aspect further.

Do you know the state of Digital Transformation in your company? If not, try to get an idea using the EACG Digital Maturity Model!

Find the right business model innovation

Well, but how to identify such a cool new business model? Assuming your current model is performing well. Your company is producing some (hundred) million turnover a year and you are happy to see a solid margin. Could you lay back and relax? Or should you hurry to take action? And what to do, if?

For sure time to act is now. Information technology will change habits and buying behavior. The earlier you try to understand and adopt, the better. Are payments executed today primarily using credit cards, could it be another micro-payment service. Are today intermediaries involved organizing fleets could it be the OEM himself, selling transport capacity in the future. The transformation of business models offers the unique opportunity to redefine the own position in the overall value chain. Probably this is THE opportunity for the coming decades. But for sure only, if you move fast enough!

At EACG we have developed the Value-Spot-concept based on state of the art management approaches and analysis techniques. It support s the strategic analysis of a company, focusing on the digital options. Coming from the position in the value chain (what am I delivering in what amounts?) and the existing custoemr groups (to whom?) as well as their current and future priorities (what are their concerns?) the future demand, respectively the most value adding service will be derived (what will I serve?) and priced (at which price?).

These results will be reflected with the own value chain position (will it be possible to establish that?), to identify acceptance and potentially required partners (whom I require for support/alliances?). This context will allow to identify future services and compensation schemes.

Stringent focus on customer groups as their priorities allows to develop and evaluate future scenarios. The scenarios build the basis for identification of required technological capabilities. Based on this understanding it becomes possible to estimate the expenses the endeavor will produce. Compared with the potential revenues resulting from the opportunity it becomes a simple decision. Do not forget the omission option in this calculation. In general this will include a decline on the current turnover. Depending on the specific case, this might be calculated as additional costs of the omission case. If the changes will avoid these losses they might also be added as additional turnover to the new model. However, in an optimal constellation the share of value creation will grow in the new model.

Giving answers to these questions takes focus, time and energy. Our experience shows that it is not possible to provide this besides the standard operational work! If not given suitable freedom, the endeavor is determined to die before it even has been born. Focus and strategy are essential to avoid expensive failures.

Collecting data, AI based analysis or decision making, blockchain approaches or automation initiatives all will keep your IT department busy. Technicians will love to dive deep into all these modern technologies. But whether and how they will pay off or even build the base for a digital future, is another story.

Modern technologies offer much opportunity to keep your IT staff busy. Goals and focus are essential to keep your initiatives economic efficient!

The Making of 365FarmNet

An interesting transformation took place at Claas. The manufacturer of harvesters and tractors identified in 2012/2013 that it become increasingly difficult to convince customers investing six digit figures into new machines, with even more horsepower. On the one hand the longevity – 30 years are nothing special – of the machines does not create demand, on the other hand the argumentation on productivity increases due to even wider working widths at already available 12 meters or improved harvesting efficiency at achieved levels above 98 percent is getting almost impossible.

Focusing on customer priorities it became visible that farmers are facing a growing number of management information systems to co-ordinate all tasks on a farm. The management process executed by the customer moved into focus; a kind of forward integration in the value chain.

By providing a SaaS solution offering a unified digital platform (s. 365Framnet) for all organizational as well as business tasks of farmer’s daily work, a kind of business driven ERP-system, Claas advances from the task taking machinery provider to the driving co-ordinator. All machinery tasks can be planned inside 365FarmNet apps and transferred to the machines for execution. Using the already existing Telemetry service machines may be monitored and execution may be adjusted, tractors for unlading the harvesters or refueling them may be co-ordinated just in time, staffing may be optimized etc. With this initiative Claas not only provided a sound business portal or ERP on demand for farmers, Claas opened up new markets and a new value proposition to its existing customers, which could be further developed an monetized.

EACG had the opportunity to support this process. Within a few months the vision became a solution, that could be presented and tested with customers.

Identify Customer Priorities

Key to the identification of this quiet unusual opportunity has been the deep understanding of the current and future challenges of the customer group farmer. The detailed insight into the daily needs and pains of the farmers helped, to identify such an approach offering new customer access and sustainably re-arranging the positions within the value chain: From machinery supplier to provider of the core management process.

Even, if it will cost quiet some time and effort: All who did not yet receive clear goals for their Digital Transformation from their customers should consider this research as relevant. We suggest to apply the EACG Value Spot model. In the first step the revenue is split into customer groups. Groups may be build based on discrete criteria such as sector (financial services, retail, manufacturing, etc.) or geographies. Some times it also makes sense to differentiate by company size, however this segmentation typically is more relevant in secondary industries (hospitality, finance, etc.).

For each of these groups the most relevant three to five topics are identified, which will dominate the agenda of the companies. Ideally the relation to your customers is good enough to just ask them. If this is not possible, you must anticipate, talk to insiders and experts. Make sure not to focus on the current priorities only but also the priorities of the coming years (t+5).

The comparison of these two lists will show how your current service will change in the awareness of your customers. If you will see your service under the top 5 priorities even now and in the future, you do not need to hurry. if it disappears from the list, you might want to consider changing the customer group in the longrun or adjusting your offering.

Jeff Bezos on the “world’s most cutsomer centric company”, insbes. Min 5:00->5:45, what to do on products that bring no revenue

(klicken zum Abspielen)

Often we are asked, which kind of crystal balls we stash in our basement, allowing us to identify future priorities. Indeed there is – unfortunately – none.Any of our anticipations will identify a Black Swan before it turns around the corner. Bt there is a set of patterns that can be applied. This includes sector specific analysis like state of competition, technology adoption or consolidation level but also models like the innovation patterns of Altschuller.(3)

This insight will be combined with the own position. What is the value of the own service in this context? Which features could be added? Where are you positioned today/tomorrow within the new shaped value chain?

Is there any capability that can support all or several customer groups applying these scenarios? If yes, this might be a future capability, which is good to focus. Provide this capability or optimize it using technology may be a good start. One benefit might be an improved cost position.

Sample Prediction for the Mail Order Business

The diagram on the left shows a development prognosis form the point of view of a online retailer that has been conducted in 2010. All by then known and reasonable technology and consumer trends were put together and extrapolated a few years in the future. This will result in new sales and value creation approaches.

For example in 2010 a very strong trend to event based and individualized offerings has been visible. A much more demand/user oriented sales approach than the so far executed catalogue focused selling. Whether it be regionalized or interest based, all together the core trick was to increase individualization of offerings. Mass data analysis (realtime click stream and order history) as well as AI will dominate the next level of sales approach.

Taking these guardrails, the need to drive an article into the correct assortment at the right time grows. Thus the need to optimize the management of article information becomes clear to be a lasting capability across several future development steps.

The assessment of all (wanted) roles, tasks and needs of all participants in the particular value net participating in such a scenario, allows to identify upcoming demand of each customer group.

Identify your own Value Spot

Having created such a picture, you may start to think about your own position within the value net. You also may identify what to sell or respectively what to charge for in which situation.

Purchase situation,specialization respectively differentiation of the services or products offered as well as the binding character are central building blocks to design such a business model. Very interesting seem to be models, that offer price elasticity, allowing to bind compensation on customer’s success. Very pleasant also are models, which allow to charge a premium after the purchase decision – so to say during the bonding phase, e.g. Fremium or “in app purchases”.

Especially in the world of data economy many models are designed to provide a basic service or information for free. This creates customer relations, customer data and customer retention. All this may be monetized in additional business cases or with value added data analysis.

As a sample refer once more to 365FarmNet. The SaaS solution for farmingoffer business services to support the work on the farm: milk management, stock management, cultivation planning, fertilizer planning, pig management, etc. This allows alternative value spots.

FarmNet decided to charge each and every single business module based on utilization, meaning per pig, acre or cow, managed by the module.

An alternative would have been to provide all modules for free to increase adoption and collect data on the real life agriculture economy. A widely spread audience is always great to establish de-facto standards. I the same time data could have been anonymized and provided as a real-time-data-analytics platform where providers of fertilizers, seeds or could study in realtime the used seeding or harvesting strategies, benchmark their goods or the required machinery. The subscription to such a data service could be quiet interesting to these providers and for sure the would be willing to pay a premium here.

Very important it is to challenge the models identified and/or preferred with relevant participants of each participating group. It could be that the preferred selection is not accepted as it produces new issues or disadvantages for some of the customers, which are not directly visible. Be sure to validate all feedback with a wider audience to avoid bias.

I always remember the story of Holland Sweetener Company (HSC)! Coke and Pepsi required NutraSweet, produced by Monsanto and sold with a very high premium. When the patent for NutraSweet was about to end, Coke and Pepsi motivated HSC to set up plant capacities to produce NutraSweet substitutes. Based on this threat, financed by HSC, both re-negotiated their contracts with Monsanto. HSC did not see a dime for its invest. (4)

Conclusion

Alltogether the current situation offers the – pometially unique – opportunity to reshuffle the value chain(s) your company is embedded in! To achive this sustainably, it will require a stringent strategy, a clear goal and dedication to achieve.

Only those who develop early a clear understanding of the upcoming value nets, will be able to cope with the coming changes. Today’s revenue sources may dry up tomorrow, due to changing or new sales approaches and customer access. To not be on one’s beam-ends, it is advisable to organize your own scenarios by time and know your options. Such an understanding builds the foundation for a sound and successful Digital Transformation. The absence of such a foundation degrades all digital initiatives to simple technical solutions or automation initiatives.

Is your Digital Transformation already running? Are you sure to be on the right track?

Further articles

This is the first of a series of articles on different aspects of Digital Transformation. Further articles will cover culture, organizational aspects, financial and technical aspects. They will be published throughout the next weeks follwoing the same format. If you want to ensure not to miss any, subscribe to our newsletter.

List of references

(1) s. Apple quarterly earnings Q1FY19, Q2FY19, https://investor.apple.com/investor-relations/default.aspx

(2) s. Jack Welch, „Was zählt“, Econ Verlag, 2001

(3) s.G.S. Altschuller „Erfinden - (k)ein Problem?“, Tribüne Verlag, Berlin 1973

(4) s. Harvard Business Manager, „Mehr Geschäftserfolg - dank der Spieltheorie“, 18. Jg. 2. Q 1996, S. 86